The transforming financial sector stands at a crossroad, faced with the challenge of aligning its operations with the broader goals of society and the environment. Despite significant progress in recent years, a glaring “purpose gap” persists, reflecting a misalignment between the sector’s actions and the urgent need for sustainable economic practices. This article explores the evolving landscape of sustainable finance, the role of regulation in closing this gap, and the necessity of a dual approach that combines top-down regulatory frameworks with bottom-up shifts in organizational culture and mindset. Within the upcoming requirements for banks to devise their climate plans under CRD VI, there is a great opportunity to trigger the necessary actions that ensure their financial stability and a sustainable transition.

A Dual Approach to Transforming the Financial Sector

The Purpose Gap: A Persistent Challenge

Banking is, at its essence, a system which facilitates the use of money for the purpose of enabling us to achieve our goals, as individuals, communities, and as societies. They are grounded in the real economy and fulfil five main functions: creating money, channelling money, looking after other people’s money, sharing risk, and maintaining transaction and settlement systems. However, as the industry grows in complexity, its profit-driven nature has progressively opened a gap between their purpose within the real economy and their private goals.

The global financial crisis in 2008 exposed how banks failed as protectors of people’s money and at managing the risk of their operation. What started as a mechanism to hedge the credit risk for real estate financing, ended up leading to speculative investments in obscure securities that created a bubble that had worldwide implications when it burst. A clear omission of their fiduciary duty in their pursuit of higher returns, and a sheer expression of its purpose gap.

As a response to this violation, the Basel Committee for Banking Supervision introduced the enhanced Basel III framework and later the CRR III and CRD VI amendments to make banks more accountable. By raising capital requirements, governance standards and increasing reporting requirements on credit exposures, the likelihood for a similar crisis to take place has been (at least partially) mitigated.

Despite this achievement, the purpose gap of banks is still wide open. During the 10 years that came after the crisis, only 10% of bank lending was directed into the productive economy, with the rest invested in property and financial markets. The banking industry must return to its founding mission of creating financial opportunity for everyone, not just for executives or shareholders. Creating this financial opportunity gains special importance as the productive system undergoes a significant transition to avert the more dire consequences of climate change.

Steering Towards Sustainability Through Regulation

Since 2008, the discussions about the stability of the financial system have evolved to include policies that address the mounting climate and environmental risks. The European Energy Agency issued a report pointing out that societal preparedness and policy implementation are lagging substantially behind the quickly increasing climate risk levels. This assessment of the 36 major climate risks for Europe indicated that almost all can reach critical or even catastrophic levels during this century under the current emissions’ trajectory, which would have severe economic impacts.

This urgency is only becoming more material every day. The 12-month period between February 2023 and January 2024 was the warmest year on record over more than 100,000 years globally, with Europe being the fastest-warming continent, warming at about twice the global rate.

The financial sector plays a key role in improving the flow of money towards sustainable activities across the European Union to mitigate these changes, and regulators are aiming to streamline this process. As the European Climate Law set a legally binding target of net-zero greenhouse gas emissions by 2050, supported by the Fit for 55 strategy to reduce EU emissions by at least 55% by 2030, the regulatory framework for the financial sector has followed suit.

While supervisors cannot define the banks’ credit portfolio, the current regulatory transformation aims to incorporate the risks of failing to decarbonize the economy into their strategy. In 2021, the Sustainable Finance Package introduced the EU Taxonomy, the Corporate Sustainability Reporting Directive (CSRD) and triggered several amendments regarding the integration of sustainability risks for banks, investment firms, insurance and reinsurance undertakings. Now, whilst the CRD VI revision awaits its final vote by Parliament after being agreed and endorsed in December 2023, banks can expect enhancements in the regulatory prudential framework to better integrate climate risks.

The making of a transition plan is climbing up the banking agenda, as supervisors evaluate the way of incorporating environmental and social factors into the Pillar 1 framework. The goal of this plan is to assess the alignment of their portfolios with the emission targets to become climate neutral by 2050. By incorporating relevant goals, measures and actions, banks are expected to address the financial risks arising in the short, medium and long term from ESG factors. Moreover, banks that fall within the scope of European Banking Authority’s Implementing Technical Standards on Pillar 3 disclosures on environmental, social and governance risks will have to disclose the Paris alignment of their credit portfolios by the end of 2024 at the latest.

Beyond Regulation: Changing Mindsets and Assumptions

The main Dutch financial institutions have already committed to goals of the Paris Agreement for their financing and/or investment portfolios, and some have already published their transition plans. However, an evaluation of the effectiveness and credibility of these action plans concluded that their strategies are still lacking clarity on emission reduction targets and fall short of the necessary ambition to achieve results of a significant magnitude. None of the analysed financial institutions achieved a pass mark for their climate plan.

Similarly, the already mentioned report by the European Energy Association analysed 95 banks covering 75% of euro area loans to assess their alignment to the Union’s climate goals. It found that banks’ credit portfolios are substantially misaligned with the goals of the Paris Agreement, leading to elevated transition risks for roughly 90% of these banks. While 70% of these banks could face elevated litigation risks as they are publicly committed to the Paris Agreement, but their credit portfolio is still measurably misaligned with it.

The misalignment of the portfolio of this banks with the goals of the Paris Agreement is a clear representation of the current purpose gap of these institutions. Regardless of the changes introduced in the prudential framework, these regulations can only go so far if the internal values have remained the same. This is not to say that there are no exceptions within the banks, but they have not become the rule yet.

This level of change will not be achieved through customer and investor demand, NGO campaigning and regulatory pressure alone – banks themselves must be supported and challenged to transform themselves from the inside out. When exploring how to transform mainstream financial institutions from the inside so they better serve people and the planet, the Finance Innovation lab identified four leverage points for change.

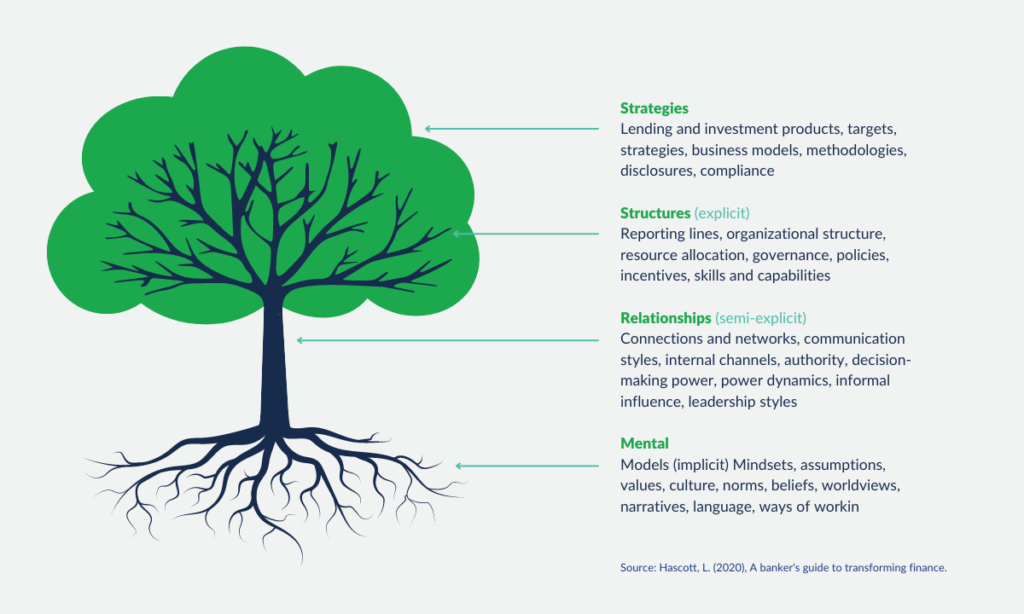

These leverage points can be visualized in the shape of a tree. Starting with Strategies, depicted as the leaves, these are the outward expressions and actions an organization adopts. They are supported and made possible by the Structures, the tree’s branches, which are the frameworks and systems put in place within an organization. These structures are determined by the network of Relationships, symbolizing the tree’s trunk, which includes how individuals within the organization connect, communicate, and distribute power among themselves. The foundation of it all, the root system, consists of Mental Models. These are the deep-seated beliefs, norms, assumptions, and narratives that underpin and influence everything above ground – from the way relationships are formed and power is shared to the structures built and the strategies pursued.

While regulatory frameworks play an important role in shaping the functioning of banks, they are not sufficient to bridge their purpose gap. The efforts of the supervisors of steering the sector towards sustainability is mainly aimed to shaping their strategies and structures, but are not fit for influencing the underlying relationships and mental models. This is the point where this top-down approach faces its main limitations.

For banks to be fit to respond to what the current context demands from them, there is a need to influence the mental models that have guided these institutions through their successes and shortfalls. An adjusted world-view and set of values are required to foster internal and external relationships guided by sustainability. However, this is not going to take place by trying to convince people to think differently.

It is by supporting those who are already influencing this leverage points from within, that the first steps towards change that have already been taken can increase in scale. Thus, this bottom-up approach complements the regulatory efforts by promoting the change agents that already exist. Agents that have already championed change through shareholder engagement in initiatives like Climate Action 100+, and through commitments of exclusion and divestment, which are already triggering corporate culture shifts.

Bridging the Gap: A Dual Approach to Transformation

Approaching the compliance process of the upcoming regulatory changes, by engaging with the change agents within the organization, can achieve long-lasting results. Some frontrunner banks have already started to use transition planning tools to measure risks in their credit portfolio stemming from the transition towards a decarbonised economy. Other banks have already started managing transition risks through active client engagement, and offering transition finance products. These examples show that while it may be challenging to accomplish ‘Fit for 55’, it is far from impossible.

Admittedly, assigning the financial sector the responsibility of a sustainable transition has triggered a debate whether this exceeds the role and purpose of these institutions. This discussion becomes quite tangible when discussing ESG investment and investor-led engagement initiatives like Climate Action 100+. These are perceived by some as disruptions to the market that distract companies and asset managers from their main goal, enlarging their bottom line. In states like Texas and Oklahoma in the United States, asset managers that integrate ESG factors in their investment policies have been banned from the state and from doing business with the government.

However, this is missing the point that sustainable finance goes beyond the field of climate enthusiasts. Incorporating climate risks in the strategy of financial institutions is a matter of impact and risk management, it is an economic reality. The referred changes in the regulatory landscape are not only about reducing the environmental impact of our current economic activities. They are about ensuring the stability of the financial system, as it is not a matter of if but of when will climate risks translate into measurable impacts in credit, market, operational and liquidity risks. The faster banks embrace the fact that mitigating climate risk has become an essential part of their fiduciary duty, the quicker we will also see a positive transformation of our economic system to a more sustainable pathway.

To achieve this, the making of the transition plans that will be required by the CRD VI are a great opportunity to have a dual approach to start shaping a better future. Taking advantage of the top-down regulatory changes to promote bottom-up cultural and mindset shifts to achieve lasting change. Nonetheless, creating an enabling environment and the necessary connections for this transformation becomes challenging while managing the business as usual.

This is where we offer our help, at RiskSphere we strive for the implementation of sustainability projects that trigger positive changes for our clients. By working with stakeholders to turn ambitious targets into real-world impacts, we help organizations not just adapt, but lead the way in sustainable practice. Contact us to see how we can help your organization make a difference across the board.

Reach out for tailored advice

Armed with a clear understanding of the applications and limitations of climate risk stress tests and scenario analysis, you're better prepared to harness their power. At RiskSphere, we are dedicated to helping you navigate the complexities of climate risk management.

Contact us